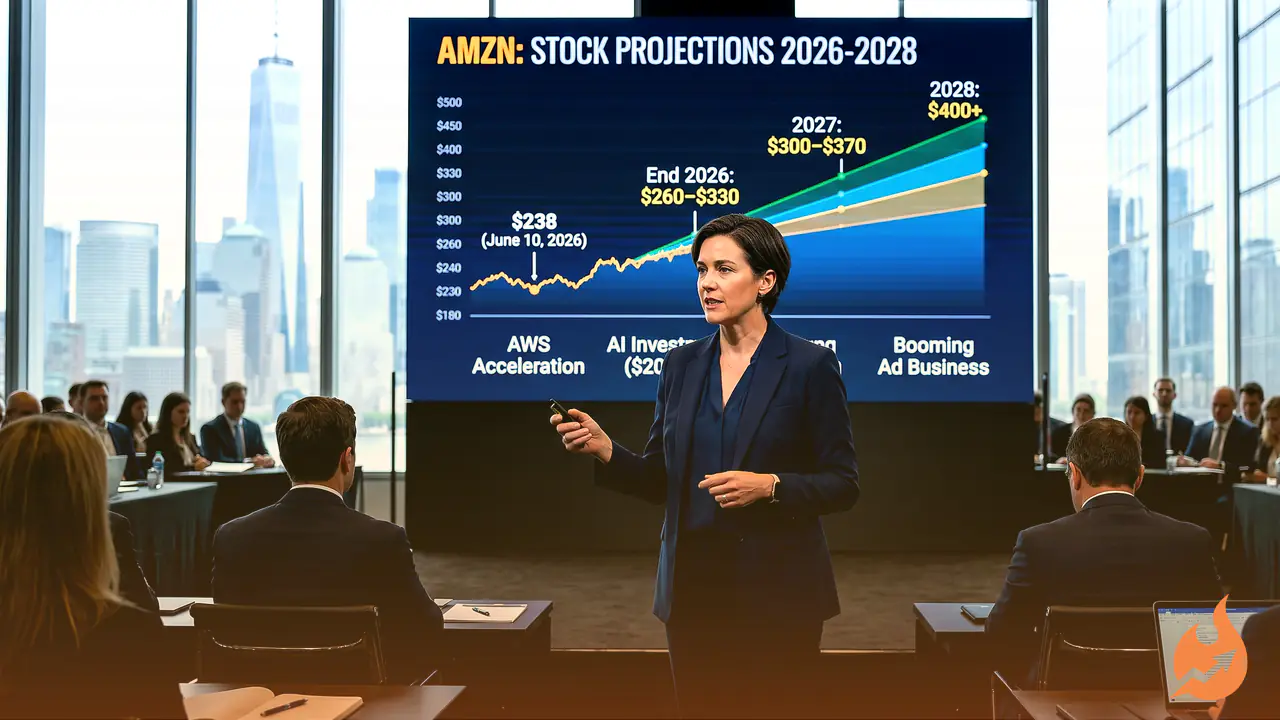

Amazon, the e-commerce and cloud giant trading under the ticker AMZN, has become one of the most closely watched bets on Wall Street. The stock closed at $238 on June 10, 2026, sitting well below its 52-week high of $278.56. From that current $238 level, the prevailing view among analysts is clear: the shares could reach a range of $260 to $330 by the end of 2026, move up to somewhere between $300 and $370 in 2027, and potentially break past $400 by 2028.

The conviction is striking. Of the analysts polled by S&P Global, 66 carry a “Strong Buy” consensus on the stock, and the average price target currently stands at $312.79. Three forces are doing the heavy lifting behind this optimism — AWS revenue that is re-accelerating, a $200 billion AI infrastructure investment, and a fast-growing advertising and subscription business that is lifting overall margins. For 2026 alone, Wall Street's range runs from a conservative $262.90 on the low end up to $330, provided earnings per share come in ahead of estimates.

What Wall Street Is Saying Right Now

Across the sell side, the tone is broadly very constructive. Truist Securities lifted its target to $320 on May 29, 2026. Mizuho holds the highest active target at $325, while Benchmark had already pushed to $370 back in April. Blending the various sources, the 12-month consensus lands between $312 and $319.

Evercore ISI's Mark Mahaney named AMZN his top large-cap pick for the year and pointed to 27% AWS growth in 2026 as a key catalyst. In his words:

“At the end of the day, AMZN remains a high-quality compounder (25% EPS CAGR), with solid double-digit revenue growth, expanding operating margins, and free cash flow likely to inflect up materially in a 24-month timeframe.”

Morgan Stanley weighed in too, after reviewing Amazon's capex plans and data center buildout. The firm set a base case of $300 and a bull case of $350, adding:

“More conviction that AWS growth has the potential to accelerate to 20%+ in ’26 — ahead of our base model and key driver of AMZN's multiple.”

The Longer Road Through 2027 and 2028

LongForecast's monthly model shows the stock recovering through most of 2027, with a projected December close of $333 — a gain of nearly 40% from where AMZN trades today. By April 2028, the same model points to a potential high of $449 and a close of $416. The broader Wall Street consensus for 2027 sets a floor above $300, with maximum targets reaching $370 if enterprise AI adoption hits full stride. Looking out to 2028, multi-year fundamental models put $400 within reach, tied to a revenue CAGR of roughly 12% and EPS compounding somewhere in the 15% to 20% range annually.

Amazon CEO Andy Jassy reinforced that longer-term case in the company's Q1 FY2026 earnings release:

“AWS is growing 28% (our fastest growth in 15 quarters) on a very large base, our chips business topped a $20 billion revenue run rate (growing triple digits year-over-year), Advertising grew to over $70 billion in TTM revenue, and unit growth in our Stores reached 15% (the highest since the tail end of covid lockdowns).”

Month-by-Month Model Projection (Low–High, Close and Change)

2026:

- June: $190–277, close $210, change -11.8%

- October: $173–214, close $188, change -21.0%

- December: $180–212, close $196, change -17.6%

2027:

- January: $182–214, close $198, change -16.8%

- June: $236–276, close $256, change +7.6%

- December: $306–360, close $333, change +39.9%

2028:

- January: $322–378, close $350, change +47.1%

- April: $383–449, close $416, change +74.8%

- June: $356–418, close $387, change +62.6%

The Big Risks to This Forecast

The single biggest source of tension in any Amazon forecast right now is that $200 billion capex commitment. Spending at that scale compresses free cash flow in the near term, and if enterprise AI demand takes longer to monetize than Wall Street's models assume, the stock is likely to disappoint the investors who are banking on margin expansion by 2027. The regulatory headwinds are real, too.

The EU is advancing cloud rules that could shut AWS out of public-sector contracts, while antitrust scrutiny lingers as an overhang across multiple markets. Competition from low-cost e-commerce platforms remains a drag on core retail margins — though most analysts' targets already assume advertising and AWS will absorb much of that pressure. Executive chairman Jeff Bezos made Amazon's direction unmistakable in a CNBC Squawk Box interview on May 20, 2026:

“My through line for the last few years has been AI. My time at Amazon is spent on AI. My time at Prometheus is spent on AI. And my time at Blue is largely spent on AI.”