For most salaried workers, a PF account is seen purely as a way to build retirement savings. But tucked alongside it is a substantial insurance cover that a large number of employees still know nothing about. The EPF scheme, run by the Employees' Provident Fund Organisation (EPFO), is counted among the country's biggest social security programmes, and its core purpose is to keep workers financially secure after they stop working.

How Money Builds Up in PF

While an employee is working, both the worker and the employer deposit a fixed amount into the PF account every month, and interest is added to this balance from time to time. Year after year this sum keeps growing, and by the time of retirement it has turned into a sizeable fund. Yet the value of EPF does not end with these future savings — attached to it is an insurance benefit that a huge number of employees remain unaware of.

EPFO 3.0 Reforms Make Services Simpler

Over the past few years, EPFO has pushed hard to make its services more digital and easier to use. The EPFO 3.0 reforms aim to give employees less paperwork, faster services and simpler account management. PF withdrawals, the claim process and several other account-related services are now far smoother than before. The direct benefit is that workers can reach their money more quickly and claims are settled in less time. With the digital platform expanding, millions of employees are now able to access many facilities from home.

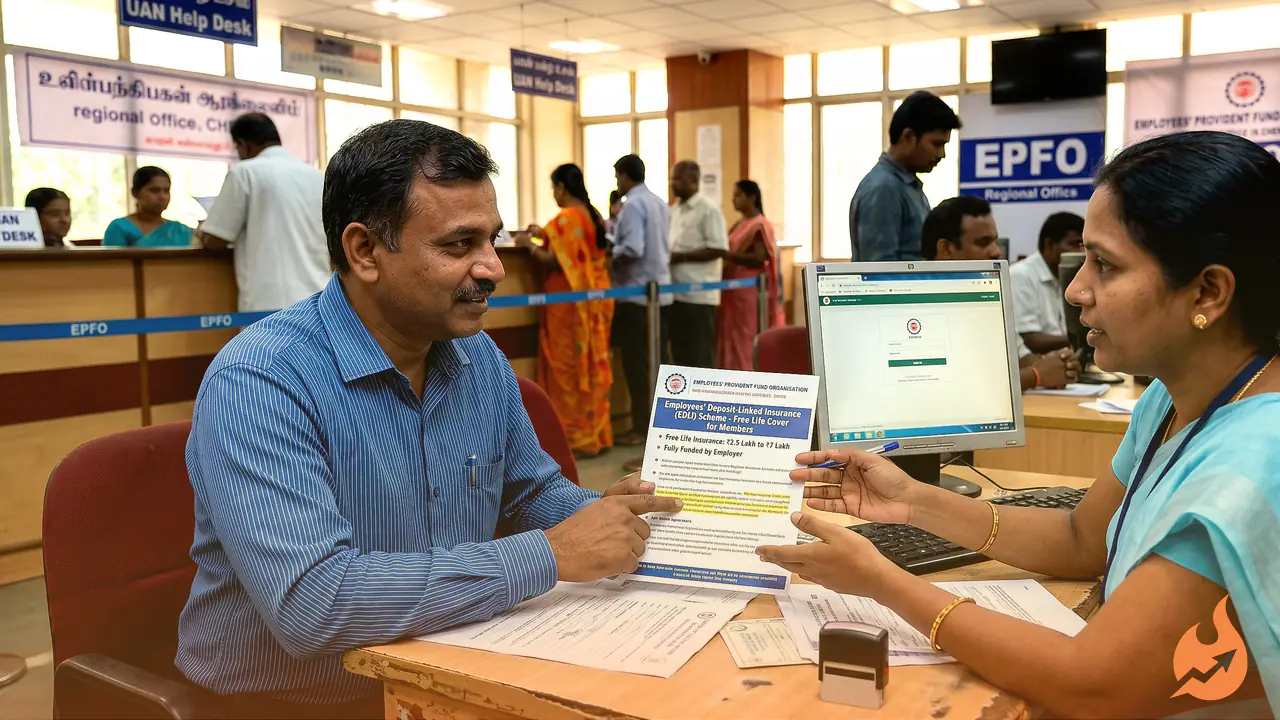

What EDLI Is and Who Gets It

This special insurance cover linked to EPF is provided under the Employees' Deposit Linked Insurance scheme, or EDLI. The key point is that it applies automatically to every eligible EPF member. There is no separate application to file, and the employee does not have to deposit any extra money. If an employee dies while in service, the person they have nominated or their family members can claim the insurance amount.

For this scheme, the employer deposits 0.5 percent of the employee's salary into the insurance fund. In other words, the entire cost of the cover is borne by the company, and the employee gets this protection completely free.

How Much the Family Can Receive

The biggest advantage of EDLI is that it gives an employee's family financial support in a moment of crisis. Under the rules, an eligible family can receive a minimum of ₹2.5 lakh and a maximum of up to ₹7 lakh. The exact amount is fixed on the basis of the employee's salary, the balance in the PF account and other prescribed standards. If a family's main earning member is suddenly gone, this assistance can prove to be a major relief. That is precisely why the scheme is regarded as an important social security measure for working people.

How the Insurance Amount Is Calculated

The benefit amount is worked out by looking at the employee's salary and the records of the PF account. Generally, the average salary of the last 12 months and the PF balance are taken into account. According to one calculation method, the insurance amount is arrived at by adding 35 times the average monthly salary (capped at ₹15,000) to 50 percent of the average PF balance. However, there is also a limit set on this additional benefit drawn from the PF balance. After all these calculations, the total payout can reach a maximum of ₹7 lakh. This ensures that the employee's family receives enough financial help when it is needed most.

Lack of Awareness Remains the Big Gap

Experts believe that awareness about this EPF-linked insurance benefit is still quite low. Most employees focus only on PF deposits and withdrawals, whereas schemes like EDLI are extremely important for protecting their families. The good news is that no additional premium has to be paid for this facility and the insurance stays active on its own. The claim process has also been made faster so that families in need get financial help as quickly as possible. Given this, every EPF member should keep the nomination details in their account updated, so that in any emergency the family can claim this benefit without trouble.