The AUD/USD currency pair is trading within a narrow range between 0.6900 and 0.6950 on Wednesday, essentially showing no movement. This lack of direction has created a period of indecision, stalling the rebound that was witnessed earlier in July. Over the last five trading sessions, the Australian Dollar has hovered near the 200-day Exponential Moving Average (EMA) at 0.6900 without finding the momentum to break away. With neither strong follow-through nor sharp rejection, the pair is currently stuck in the middle of last week's trading range, creating a sense of suspense rather than stability after a significant drop in June.

Impact of Federal Reserve Minutes

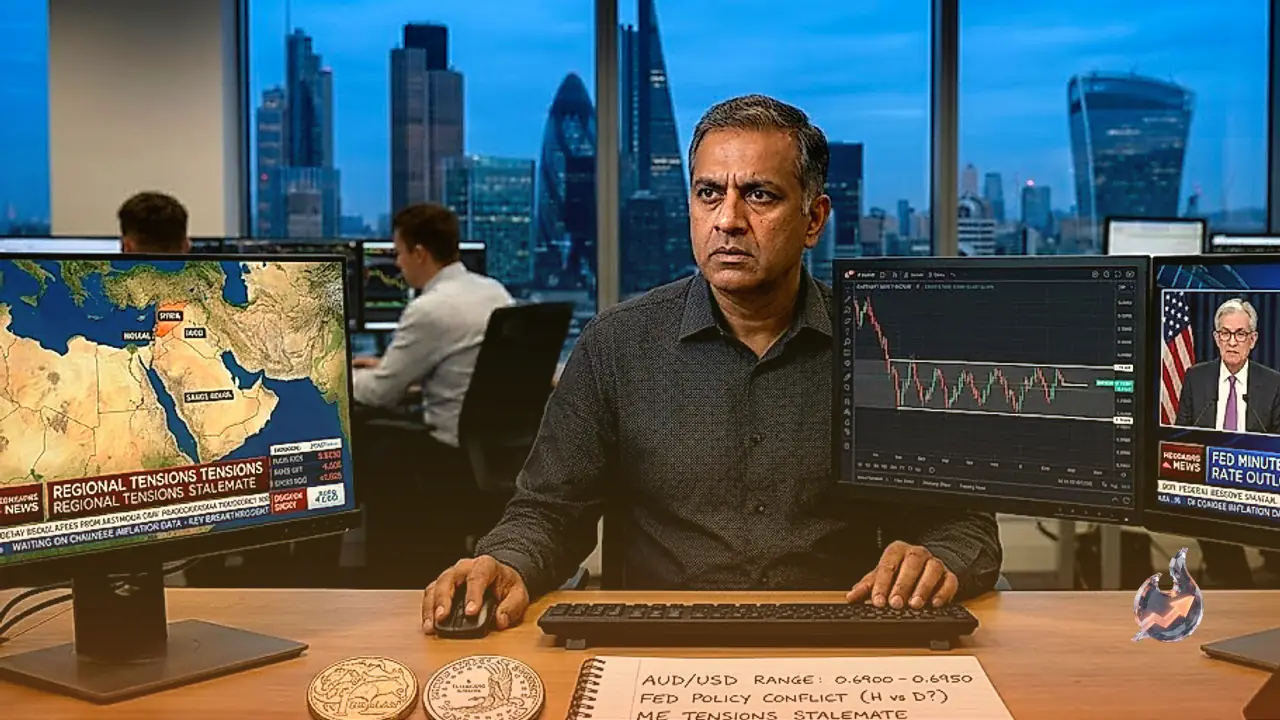

The release of the Federal Open Market Committee (FOMC) minutes on Wednesday revealed a committee deeply divided regarding future policy moves. The June dot grid showed nine officials favoring rate hikes, eight preferring to hold steady, and one calling for a rate cut. This lack of consensus keeps the US Dollar well-supported on any minor dips, which in turn acts as a ceiling for risk-sensitive currencies like the Australian Dollar. While the central bank maintains a hawkish tone, its hesitation to take immediate, definitive action provides a support floor for the currency without providing a catalyst for upward movement.

Geopolitical Tensions and Economic Offsets

Under normal market conditions, a combination of fresh US strikes on Iran and a surge of more than 6% in Crude Oil prices would typically trigger a sell-off in risk proxies like the Australian Dollar. However, because Australia is a major energy exporter, the terms-of-trade effect helps to offset the negative sentiment from the risk-off environment caused by the conflict. This unique dynamic has left the market in a state of paralysis, where the currency does not fully benefit from the war dividend nor does it suffer entirely from the flight to safety, resulting in the flattest price action of the month.

The Critical Role of the Chinese Economy

The commodity premium for the Australian Dollar is heavily filtered through Beijing's economic performance. Iron Ore remains the most significant export influencing the currency's pulse, rather than energy. With Chinese construction demand absorbing its own energy-related shocks throughout the year, the potential windfall for Australian exports has been significantly blunted. Technically, the decline from the May peak of near 0.7300 continues to dominate the chart. The sideways movement forming beneath the falling 50-day EMA above 0.7000 suggests that the current consolidation might be a distribution phase in disguise rather than a foundation for a new rally.

Thursday's Data to Break the Stalemate

Market focus is now shifting to China's Consumer Price Index (CPI) data, scheduled for release on Thursday. Economists expect the annual CPI to ease to 1.1% from 1.2%, with a monthly decline of 0.2% predicted. Conversely, the Producer Price Index (PPI) is forecast to accelerate to 4.1% from 3.9% as increased input costs from global conflict filter through to factory gates. A scenario where consumer prices fall while producer costs rise points toward a margin squeeze, reflecting a difficult path for recovery. A downside surprise in the CPI will likely embolden bears to test the 0.6900 level, while an upside surprise might keep the pair trapped in this current range for another week.

Technical Levels and Outlook

With the current price sitting at 0.6933, the 0.6950 level remains the immediate resistance cap. Bulls will likely find it difficult to gain control until this zone is decisively broken. On the downside, the 200-day EMA at 0.6900 serves as the critical support, with the 0.6850 level waiting below as a secondary floor. The outlook remains bearish as long as the pair is capped below 0.6950, and a daily close below 0.6900 would likely signal a resumption of the June downtrend.